D

The doctor loan, without the small print.

A physician mortgage loan lets new and practicing doctors buy a home with little or no money down, no PMI, and an offer letter in place of pay stubs. We’ll explain what it is, who qualifies, and how to tell a real program from a repackage.

0-10%

Down payment

$0

PMI required

50+

States covered

SPECIMEN DISCLOSURE

Physician Loan Program

Down payment

0 to 100% financing common

0-10 %

Private mortgage insurance

Saves $40k+ over life

$0/ mo

Proof of income

No pay stubs required

Offer letter

Student loan treatment

IBR / PAYE accepted

IDR -aware

Close before first day

Move once, not twice

90 days early

- 27lenders in network – verified

$40k+ avg lifetime PMI saved

0% down available, up to $IM

Offer letter accepted 90 days early

IBR/ PAYE student-loan payments accepted

IN THIS REFERENCE . 7

CHAPTERS

A start-to-finish read on the physician mortgage — what it is, who qualifies, the honest math, and how to use it without getting hurt. About a fourteen-minute read.

01

Definition

02

How it works

03

Eligibility

04

Pros & cons

05

Compare

06

Afford

07

Guardrails

01

DEFINITION

What is a physician mortgage loan?

The plain-English version. A loan product a handful of banks created for doctors — designed around an offer letter and a student-loan-heavy balance sheet, not around the standard W-2 underwriting box.

A physician mortgage loan is a portfolio mortgage built by a small number of banks specifically for physicians and a handful of other high-credential professionals.

The bank keeps the loan on its own balance sheet, which means it can rewrite the rules everyone else has to follow. In a conventional mortgage, the lender plans to sell the note to Fannie Mae, Freddie Mac, or a similar agency.

To do that, the file has to match the agency’s box — two years of W-2s, a debt-to-income ratio under 43%, and a down payment large enough to avoid private mortgage insurance.

Most new doctors don’t fit that box. They have a six-figure offer letter that hasn’t started paying yet, six figures of student debt on income-driven 90 days early.

VERIFIED repayment, and no down-payment savings. A real doctor mortgage program takes those facts as a given and underwrites around them.

There are four mechanical things a real program will do that a conventional loan won’t. They’re listed on the right — and hey show up, in writing, on the closing disclosure.

THE FOUR RULES

What a real program does

i Closes on an offer letter

Up to 90 days before your first day of work — with no pay stubs required.

.

ii Uses your IBR/PAYE payment

Or 0.5-1% of balance — not the fully amortized number.

.

iii 0-10% down, no PMI

Up to high loan amounts covering most metro markets.

.

iv Underwrites for physicians

Income trajectory is recognized as unusually predictable.

02

HOW IT WORKS

The three things a real program actually does.

Each one is acolumn on your closing disclosure. If your lender can’t produce it in writing, the program isn’t a real physician loan — it’s a conventional loan wearing the label.

i. Down payment

O-10%

Little or nothing down

A real physician program funds 90—100% of the purchase price up to high loan amounts. You bring earnest money and closing costs — not a year of saved-up cash you don’t have yet.

ON THE DISCLOSURE . DOWN PAYMENT 0-10%

ii. Mortgage insurance

No PMI

No private mortgage insurance

Less than 2 down on a conventional loan typically adds $150-$400/mo in PMI. A real doctor loan eliminates it entirely — saving most borrowers $40k+ over the life of the loan.

ON THE DISCLOSURE . PMI = $0

iii. Income proof

Offer letter

An offer letter is your income

A real program funds up to 90 days before your first day — using the signed contract from your hospital, group, or fellowship as proof of income. No stubs, no W-2s.

ON THE DISCLOSURE . EMPLOYMENT OFFER

03

ELIGIBILITY

Who qualifies for a doctor loan?

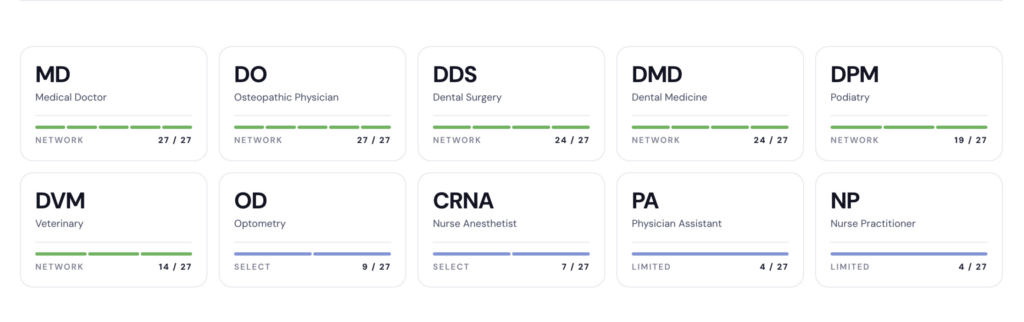

Eligibility is by credential, not by guess. Lenders publish the exact degrees and career stages they accept. Below: the credentials in our network, with answers to the questions readers actually ask.

FROM THE INBOX

Common questions, frankly answered.

A.

Yes. Most real programs will write a loan to a resident, fellow, or attending. Residents and fellows are typically capped at lower loan amounts (often $750k-$1m) because the income is lower; attendings get the full envelope.

Q.

Can I qualify during residency or fellowship?

A.

A real program will use your actual income-driven payment (IBR/PAYE/REPAYE), or 0.5-1% of the balance — not the fully amortized number a conventional lender uses. That single rule is the difference between qualifying and not qualifying for most new physicians.

Q.

What about my student loans?

A.

Most programs want a 700+ middle score, with best pricing at 740+. A 680 will still typically qualify at a small rate adjustment. Below 660, fix the score first — it’s the highest-leverage three months of your financial life.

Q.

What credit score do | need?

A.

Yes — no lifetime cap. Most physicians use a doctor loan twice: once for a residency-city starter, then again for an attending home. Some programs even allow it on a refinance or second home, though rates are higher.

Q.

Can I use a doctor loan more than once?

04

HONEST TAKE

Is the doctor loan actually a good idea?

Yes — if you treat it like a tool, not a trophy. The product is good. The most common way to get hurt with it is to use the bigger qualifying amount to buy a bigger house. Read both columns.

For .05

In the right hands – why it works

You buy with the money you actually have

No 12-month savings sprint to get to 20% down before you close on the house you've already moved to.

PMI disappears

Skipping mortgage insurance saves the average borrower $40,000+ over the life of the loan — a real, in-pocket number.

Your student loans don’t lock you out

The income-driven payment, not the fully amortized one, drives your debtto-income ratio.

The bank treats your offer letter as income

You can close before day one — up to 90 days early — meaning you move once, not twice.

The price is competitive

A real program typically prices within 0.125-0.375% of a conventional 20%- down loan. PMI savings usually erase the gap.

AGAINST – 05

Where it goes wrong – how to avoid it

It pre-approves you for more house than you should buy

A bigger qualifying number is not a bigger budget. The same trap as any first-time buyer, just at a higher dollar amount.

You start with little or no equity

If you have to sell in two years, you'll likely write a check at closing. Don’t use it for a house you'll outgrow in 24 months.

The rate is slightly higher

Expect 0.125—0.375% more than a 20%-down conventional. Worth it if you'd otherwise pay PMI; not if you have the cash.

Some repackages charge fees a conventional won't

Real ones don’t. Always compare line-by-line on the Loan Estimate, not just the headline rate.

An ARM is still an ARM

Don't take a 5/1 ARM unless you have a specific, dated plan to refinance or move before the reset.

05

COMPARE

Doctor loan vs. conventional, line by line.

Six rows decide whether the physician program is the right move for you. Run your situation against the table. If three or more rows favour the physician column, the math is on your side.

OPTION A. RECOMENDED

Physician loan

DOWN

O-10%

100% financing common up to high loan amounts

PMI

$0 / month

No private mortgage insurance, ever

INCOME

Offer letter accepted

Close up to 90 days before first day of work

SL DTI

IBR / PAYEused

Or 0.5-1% of balance — not fully amortized

RATE

Slightly higher

+0.125 to +0.375% vs. conventional

KNOWS MDS

Yes — specifically

Offer letters, RVUs, locums, 1099 — all familiar

vs.

OPTION B - STANDARD

Conventional w/ 20% down

DOWN

20% required

..to avoid PMI on a standard conforming loan

PMI

$150-$400 / mo

Until 22% equity, if less than 20% down

INCOME

30 days of stubs

Often a full month after you start work

SL DTI

Fully amortized

Often the difference between approve and decline

RATE

Slightly lower

..jf you actually have 20% to put down

KNOWS MDS

No — generic box

File kicked out on anything non-standard

06

AFFORD

How much can I actually afford?

The honest answer is smaller than the qualifying answer. Most physicians do well at 2x gross income on the first home and no more than 28% of gross income on principal, interest, taxes, and insurance combined.

Slide your real numbers in.

A back-of-the-envelope estimator using the “28% of gross” rule with realistic taxes, insurance, and a 6.75% rate for a 30-year doctor loan. Planning tool, not a pre-approval.

07

GAURDRAILS

Should you really do this?

Use the doctor loan if you can answer “yes” to all four. If a question lands as a “no” or a “maybe,” rent another year. The product will still be here when you’re ready.

01

Will you stay in this market for at least five years?

A doctor loan starts with little or no equity. If you sell in year two, you’ll likely write a check at closing — a five-year horizon turns that math from a coin flip into a near-certainty.

YES

5+ yr horizone

NO

Rent another year

02

Is the payment under 28% of gross income?

That’s the line where physicians comfortably absorb the cost of a house and still save 15-20% of income. Above 35%, the budget gets tight fast — especially if you’re still paying down loans.

SAFE

PITI < 28% gross

DANGER

PITI > 35% gross

03

Do you have an emergency fund?

Three to six months of expenses outside of the down payment, in cash. A doctor loan is a great product. It is not a substitute for liquidity when the water heater dies in month three.

HAVE

3-6 months, cash

NOT YET

Build first

04

Have you compared two real lenders, side by side?

Pricing varies more across “physician” programs than across conventional ones. A real program comes from a bank that holds the note; a repackage comes from a broker shopping a wholesale wholesaler. Get two Loan Estimates.

GOT

2 Load Estimates

ONLY ONE

Get a second

TAKE THE NEXT STEP

Done reading? Pick Your move

MD Mortgage Loan is the education side of the Dr. HomeFinance ecosystem. Whether you need a lender, a realtor, or an investor — one of these doors is the right one.

01.

FOR BORROWERS - FIND

Find physician-focused banks

Match with a bank-direct lender from our verified Dr. HomeFinance network — the real programs only, no broker repackages.

02.

FOR HOUSE HUNTERS FIND

Match with a physician-focused realtor

Realtors who have actually closed for doctors before — familiar with move-once timelines, fellowship contracts, and dual-physician offers.

03.

FOR INVESTORS - BUILD A PORTFOLIO

Looking to invest?

Match with a bank-direct lender from our verified Dr. HomeFinance network — the real programs only, no broker repackages.

MD Mortgage Loan

A plain-english education resource for physicians, dentists, and other high-credential professionals shopping for a real doctor mortgage.